|

| home > Introduction |

|

| V. History of Real Estate Securitization | |||

|

The following is a review of the development of real estate securitization in Japan. 1. The Budding of Real Estate Securitization Some people trace the start of present day real estate securitization back to mortgage securities that appeared in 1931 or the housing loan debt trusts of 1973, but generally securitization, in its present form, started in 1987 with the formation of small lot real estate trust beneficiary interests and the real estate conversion loans of JNR Settlement Corporation in 1990. Either way, the history of real estate securitization follows the first attempts to transform real estate from being an expensive real asset that with fixed location into small assets that can be easily traded on the securitization markets as they exist today. |

|||

2. Small Lot Real Estate Investment Products The small lot real estate investment products that appeared in 1987 were basically real estate divided into small ownership units and sold in units small enough for retail investors to purchase. The small units were developed because the generally large investment size required for real estate and its low liquidity made it difficult for retail investors to invest. These investments differed from traditional, direct real estate investment because the operator controlled the equity of each investor so that it was effectively a collective investment structure for real estate. However, it lacked any measures to protect the interests of the investors and so many investors suffered large losses after the collapse of the bubble. As a result of these losses there were calls for a legal system to be established to protect investors, and the “Real Estate Syndication Act” was enacted in April 1995 with this aim in mind. This was the foundation for real estate syndication products and led to the further development of asset monetization. |

|||

3. Asset Securitization Parallel to the development of small lot real estate products studies were proceeding on asset monetization and securitization as part of the reforms to the Japanese financial system. The first changes came in June 1993 with enactment of the “Law Concerning Regulations for Businesses Involving Specific Credit Obligations” which is commonly known as the Specific Debt Law). The Specific Debt Law established restrictions on liquidity limited to specific debts such as lease debts and credit debts, and the subsequent revision of Specific Debt Law in April 1996 made it possible to issue asset-backed securities (ABS) in Japan. In 1998, the Financial System Reform Laws were enacted as part of the financial big bang. One of the laws enacted, with great anticipation for its impact on the disposal of non-performing loans, was the “Law on Securitization of Specific Assets by TMKs” (commonly known as the former SPC Law). This law was the first law enacted to provide for comprehensive asset securitization in Japan and real estate specifically identified in the law as an asset that could be securitized (the law limited assets that may be securitized to those specifically listed). The fact that a legal framework had been established for securitizing assets was very important, but the procedures the law imposed were complex and reporting and other obligations under the law were onerous for the participants to meet. To rectify this complexity and promote securitization, the law was revised and the new law was called the “Law on Asset Monetization” (commonly known as the Asset Monetization Law). This law was enacted in November 2000 and remains in force today. The Securities Investment Trust Law was revised in 1998 to provide for “company” trusts (described later) and was named the “Law Concerning Securities Investment Trusts and Securities Investment Corporations.” After a further revision of the law in November 2000 it was named as the “Investment Trusts and Investment Corporations Law” and is commonly referred to as the Investment Trust Law. This law regulates the direct management of real estate as an investment product. Thus, basic laws for asset monetization and asset management were firmly established by 2000 and the legal framework was in place for creation and regulation of the securitization conduits (vehicles) for real estate securitization -TMKs, investment corporations and investment trusts. |

|||

4. Development of Securitization and the Financial System Here we will switch our view to the financial system and look at the development securitization has gone through. 1) Round Tables and Position Paper on Disputed Issues regarding

the Flow of New Financing Market financing is a new form of system for channeling money from the providers of capital to the users of capital. In this system the providers of capital, in many cases, are household savings introduced into the capital market via financial products and financial service companies that transfer the capital to the securitization vehicles and companies in need of capital. 2) The First Interim Report by the First Subcommittee of the Financial System Council Another key point from the committee's report was that collective investment schemes should be encouraged and play a vital role in the financial markets. A collective investment scheme is where a third party who specializes in managing funds gathers monetary investments from investors, and invests those funds to generate cash flow and/or capital gains for the benefit of the investors. Collective investment scheme is a term that encompasses the whole framework of joint investment and passive investment. In the committee's report collective investment schemes were divided into two categories: a. Asset management schemes where the investment funds are gathered from multiple parties, pooled and managed by investing in various assets, and b. Asset monetization schemes where cash flows generated by qualified assets are structured into a single or multiple investment products and sold to multiple investors. 3) The Second Interim Report by the First Subcommittee of the Financial System Council 4) Present and Future Trends The Program seeks the establishment of a regulatory framework that promotes the development and distribution of a diverse range of high quality financial products and services. This will also help achieve the goal of the expansion of financing methods that do not rely excessively on real estate collateral and guarantees and has helped fuel expectations of an expansion in real estate securitization methods. The establishment of an Investment Services Law (provisional name) is indicated as a future goal in the sections that discuss the development implementation of investor protection rules that reflect financial conditions and that will enhance the market functions and improve investor confidence in the markets. This Investment Services Law has been debated by the First Subcommittee of the Financial System Council. The First Subcommittee of the Financial System Council announced the framework of the Investment Services Law on December 22, 2005 as “In Preparation for the Investment Services Law (tentative name).” The report outlined the aim and objective of the Investment Services Law in the following manner. 1. Thoroughly Implement Rules to Protect Users and Improvement of Convenience

2. Securing Market Functions to Prepare for the Shift “From Savings to Investment”

3. Appropriate Measures for the Internationalization of Financial and Capital Markets

4. Need for the Investment Services Law (tentative name)

5. Basic Framework of the Investment Services Law

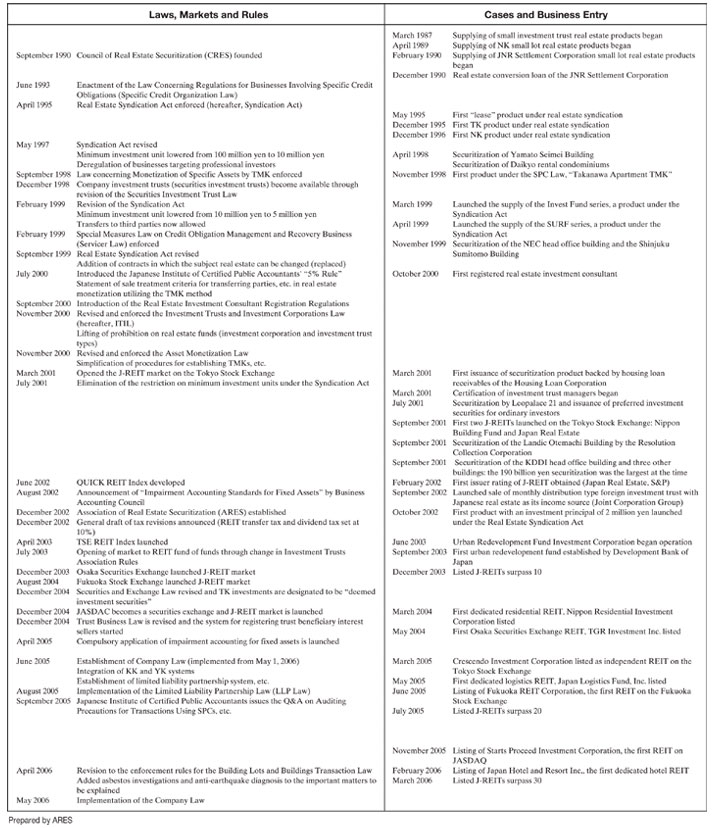

Later, the tentatively named Investment Services Law was formally named the Financial Instruments and Exchange Law and was submitted to the 164th ordinary session of the Diet in March 2006 as the Financial Instruments and Exchange Law Bill. As of the end of March 2006, the Diet debates are underway towards implementation from 2007. Figure 1-12 Chronology of the Development of Real Estate Securitization *Click the image, large size is available  |

|||

|

|||