|

| home > Introduction |

|

| IV. Significance of Real Estate Securitization | |||

|

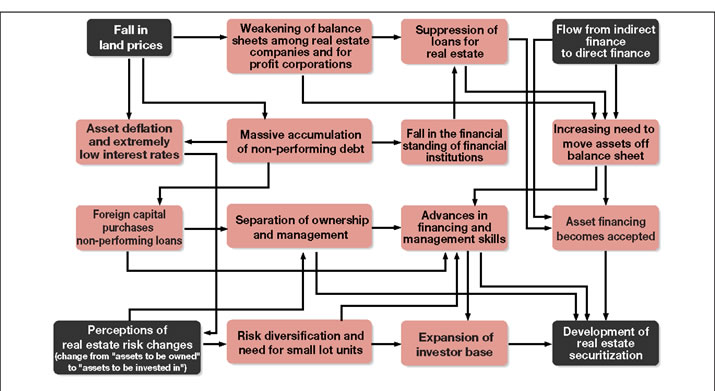

There are a number of reasons why real estate securitization has grown rapidly in the past few years while its fundamental structure and systems have remained unchanged. One of these has been the greater awareness to the risks of owning real estate. This has been amplified by the drop in land prices that began in the early 1990s and the major shift from indirect financing in the financial and capital markets to direct financing (Figure 1-8). The drop in real estate prices and emergence of massive amounts of non-performing loans led to a significant weakening of many Japanese businesses and financial institutions and contributed to further asset deflation. The monetary authorities responded with an unprecedented period of ultra-low interest rates. Against this economic backdrop, companies became more focused on financial performance and scrutinized their ownership of real estate. This scrutiny led many companies to seek to separate the responsibility for real estate ownership and management. Concurrently financial institutions began to be more cautious in extending loans to the real estate business, which resulted in fewer companies looking to acquire real estate from the mid-nineties, and the real estate market began to shrink. Figure 1-8 Background to the Development of Real Estate Securitization *Click the image, large size is available  New business models were developed around the same time focused particularly on the disposal of non-performing loans; many of these participants in this new market were backed by foreign capital, which led to major revolution in financial control and management methods. These market developments combined with the regulatory changes associated with the financial big bang, led to a shift in the financial system from indirect finance to direct finance and companies with poor credit began to focus on asset financing rather than traditional borrowing. During this period real estate securitization in Japan grew significantly and matured from merely investment real estate to financial products. This all occurred following the collapse of the “land myth and land standard system” that had been prevalent in Japan |

|||

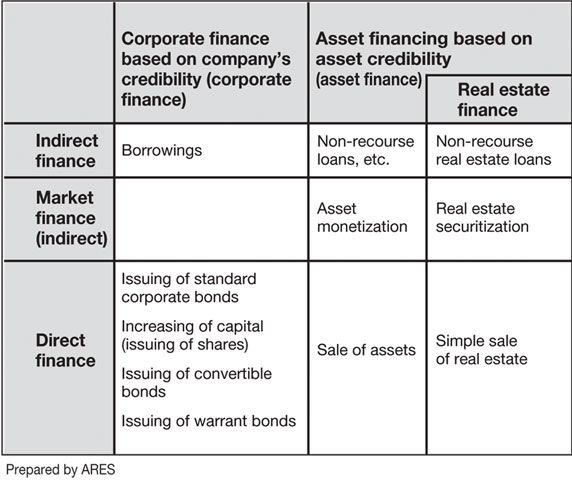

1. Corporate Finance and Asset Finance Historically in Japan corporate fund raising, or corporate finance, has depended on the credit strength of companies. Corporate finance can be further subdivided into loans from financial institutions, issuing of corporate bonds and other debt instruments to procure funds from the capital markets (debt finance) and equity finance where further equity or equity-linked instruments are issued to the capital markets. Put another way, corporate finance deals with activities that affect the right side of the balance sheet (equity and liabilities) and in many cases the assets from the right side of the balance sheet become assigned as collateral for the loans. In certain cases the personal assets of a guarantor may be subject to assignment if the owner becomes a guarantor of a loan. By contrast, asset finance is capital raising that is dependent on the credit worthiness of a specific asset owned by a company or securitization vehicle. In asset financing the asset is separated from all other assets of the operating company (thus the credit of the operating company) and funds are procured based solely on the performance of the assets that have been separated. This process, sometimes referred to as moving off balance sheet, can be applied to non-fixed asset such as accounts receivable as well as fixed assets the company owns of which real estate securitization also is a subset. The sale of an asset and receipt of sales proceeds would also be a form of asset finance under the definition above, however with the changes in the real estate market it has become more difficult to simply sell real estate to another single purchaser. This makes securitization, which provides liquidity, an essential part of the real estate market (Figure 1-9). Figure 1-9 Corporate Finance and Asset Finance *Click the image, large size is available  |

|||

| |||

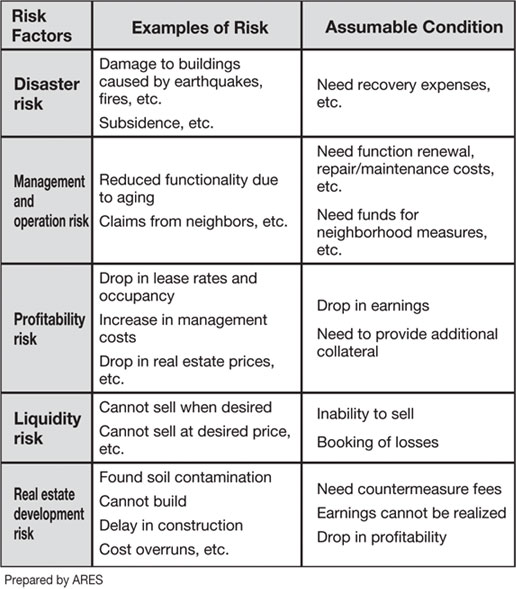

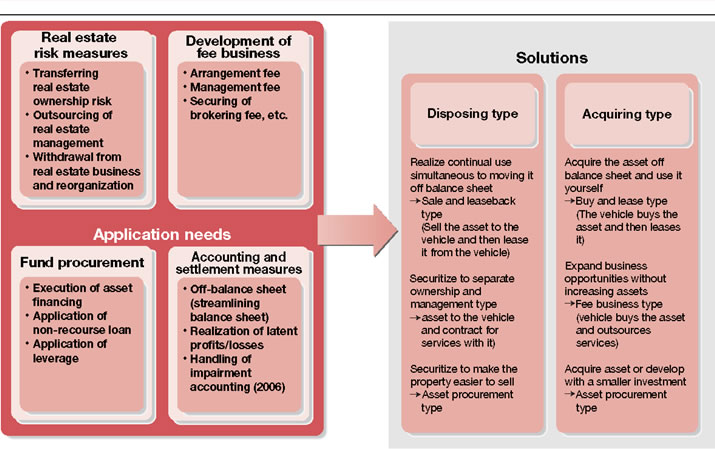

2. Objectives and Merits of Real Estate Securitization The following is a compilation of the objectives and merits of real estate securitization. 1) Fund Procurement Unlike real estate financing for an operating company, real estate securitization does not depend on the creditworthiness of the originator. This is of material advantage in many situations as funds can be procured for the originator without reducing the asset efficiency plus securitization is a real option for companies with poor credit standings to raise capital on advantageous terms provided that the real estate being securitized is of good quality. 2) Providing Liquidity to the Real Estate Market 3) Risk Transfer Many companies are not interested in bearing these risks; therefore, it is beneficial to originators if they can transfer these risks to a third-party investor via securitization. The securitization process transfers some or all of the risks of ownership from the owner to the investors. The securitization vehicle is structured to re-apportion the risks to various investors, insurers and other related parties depending on the level of risk they are each willing to assume. From the investor perspective, real estate securitization expands the range of investment choices and opportunities and with increasing numbers of investors the efficiency of the market improves. Figure 1-10 Example of Various Risks related to Real Estate *Click the image, large size is available  4) Improved Financial Standing If a company obtained assets during the bubble period of the Japanese economy and thus increased gross assets on its balance sheet, securitization will help the company improve its return on assets ratio, as the assets will be valued at market prices. In the late 1990s there were many examples of real estate securitization being used to improve the financial standing of companies. 5) Fee Business Figure 1-11 is a compilation of application needs and solutions concerning real estate securitization. The solutions that securitization offers can be divided into two patterns: 1) Using securitization vehicles primarily to dispose of real estate, and 2) Using securitization vehicles primarily to acquire real estate exposure. Figure 1-11 Application Needs and Solutions for Real Estate Securitization *Click the image, large size is available  | |||

|

|||