|

| home > Introduction |

|

| I. Basic Structure of Real Estate Securitization | |||

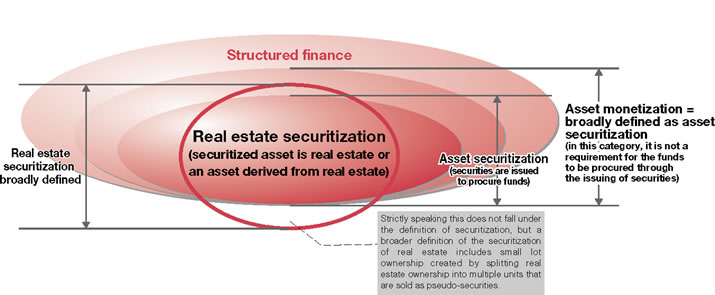

1. Securitization and Monetization Asset securitization is where a financial institution or other business that owns assets places those assets in a structure so that the risk and rewards of owning the asset are transferred to a third party. More specifically this is done by placing cash generating assets in a bankruptcy remote vehicle and implementing control functions on the asset in order to maintain its creditworthiness. Investment products that possess greater liquidity characteristics than the underlying assets, such as investment securities, are then issued backed by the securitized assets and cash flows those assets generate. There are many terms that have similar meanings in this area of finance; “securitization” is the most common but there is also “monetization” and “structured finance.” The term “monetization” is sometimes used to indicate transactions that do not lead to the issuing of investment securities as well as more sophisticated structures that include issuing publicly distributed investment securities as a means to distinguish these from investment securities under the Securities and Exchange Law. Ordinarily, “asset monetization” is used when transforming assets with low liquidity into a structure where investors can have greater liquidity. Usually this is where someone owning assets establishes an entity solely for the purpose of owning these assets (that entity is commonly called a special purpose entity or SPE) and transfers the assets to the SPE. Investment into the SPE and borrowings by the SPE, backed by future cash flow generated by the assets, can be secured and these funds flow back to the original owner. In a case like this the issuing of investment securities is not of particular importance. This is also called broad asset securitization. Structured finance is often interpreted to be more sophisticated than broad asset securitization and used to indicate financial methods that involve unique structures (Figure 1-1). Figure 1-1 Overview of Securitization and Monetization Concepts *Click the image, large size is available  In this book, the terms securitization and real estate securitization are used to indicate the broad forms of asset securitization in which the securitized asset is real estate or an asset derived from real estate (real estate backed debt, etc.). However, please note that the term real estate securitization is sometimes used for securitization or monetization in cases such as when real estate ownership is divided into small lots and sold. |

|||

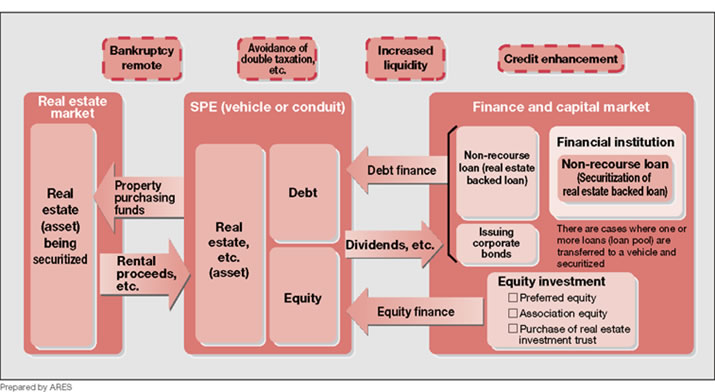

2. Basic Securitization Structure Securitization is the process that links the economic performance of any asset with the financial and capital markets. The Book “Corpus Juris Finance: Part 2” edited by the law firm Nishimura & Partners describes it in the following manner: “A technique for restructuring the cash flow of assets for which there is limited liquidity or cash flows generated by combinations of assets that, after the restructuring, creates investment products worthy of investment in accordance with the demand of investors and participants in the capital markets.” Generally there are four basic elements to securitization: (1) Assets generating the cash flow that are to be securitized (underlying asset), (2) Investors that invest in the cash flows generated by the underlying asset, (3) SPE that functions as the conduit linking the underlying asset and investors (often referred to as a special purpose vehicle (SPV)), and (4) The securitization product which represents the rights the investor will purchase and does not necessarily have to be an investment security. The transaction that combines these elements and makes the underlying asset bankruptcy remote from the previous owner of the underlying asset (originator) and any of the new investors and techniques for controlling various other risks are referred to as securitization. Among the various forms of asset securitization, real estate securitization is where investment is solicited by pledging the distribution of cash flows generated by the real estate to investors, or a means for securing greater liquidity for real estate assets that are generally considered to have low liquidity due to high transaction costs. The liquidity is secured by issuing equity interests in small denomination and these have various rights for receiving cash flows generated by the securitized real estate. Figure 1-2 outlines the basic structure of real estate securitization, but securitization is not limited to the very simple model indicated here. Many variations have been developed that show both great diversification and increasingly complex structures. Figure 1-2 Basic Structure of Real Estate Securitization *Click the image, large size is available

|

|||

3. Basic Requirements for Real Estate Securitization Real estate securitization needs to fulfill a number of requirements. The below summarizes the requirements. 1) Bankruptcy Remoteness As mentioned previously, the originator transfers the underlying real estate asset into an SPE in the first stage of the securitization process. However, if the originator were to go bankrupt after transferring the asset to the SPE and the bankruptcy administrator or creditors were to try to seize the securitized asset, a very unstable situation would arise where investors would not receive the earnings they expected and the redemption of the principal would be impossible. Therefore, it is important to establish each SPE as bankruptcy remote from the originator so that investors do not suffer needless loss. Even if the asset that is securitized is remote from any bankruptcy proceedings of the originator there is still the risk that the securitization vehicle goes bankrupt and a default occurs. Consequently, it is essential to have some bankruptcy prevention measure in place for the vehicle. (See Chapter III. 1. Legal Considerations for bankruptcy remoteness.) 2) Double Taxation In order to avoid double taxation a system has been developed where securitization vehicles based on specific securitization laws enable dividends to be recognized as expenses provided certain conduit criteria are met. However, this does not mean that double taxation is avoided unconditionally so there is a need for operational awareness. (See Chapter III. 2. Tax Points for Details on avoiding Double Taxation.) 3) Credit Enhancement for Controlling Risk When structuring a real estate securitization product it is common to include a form of credit enhancement to increase the credit worthiness of the security and to better meet the demands of investors. Internal credit enhancements features that use the cash flow of the securitized asset include creating a split capital structure that will include preferred and subordinated securities that will have different rights to the asset's cash flow and may also include a seller reserve whereby the seller will leave a cash reserve from the sales proceeds in the securitization vehicle. External credit enhancement measures include cash collateral and guarantees provided by third parties. a. Preferred/Subordinated Structures Ordinarily, the most subordinated investments are equity and are invested into the securitization vehicle through a Tokumei Kumiai (TK) or preferred equity investment. The preferred portion of the capital structure may be further divided into several segments and corporate bonds with varying credit ratings are issued, this is commonly referred to as tranching and refers to the division of the credit portion of the investment according to their respective risks and each portion is called a tranche. b. Seller Reserve c. Cash Collateral d. Guarantees from a Third Party 4) Providing Liquidity 5) Information Disclosure There are already regulations provided for in various laws that protect investors in real estate securitization products. However, it is important that not only legal requirements are met but also that information disclosure be consistently maintained so that investors can continually make informed decisions and take responsibility for their investments. |

|||

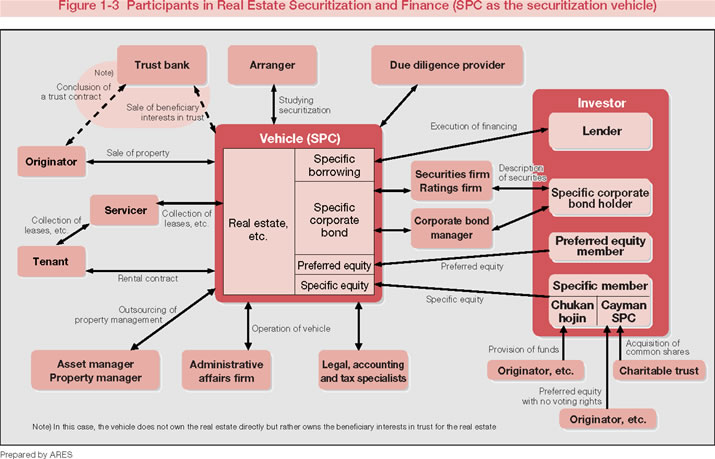

4. Real Estate Securitization Market Participants One characteristic of real estate securitization is that it fuses the real estate business and finance but makes a clear distinction between the various functions and has created a further division of functions. In response to this trend for clearer distinction between the functions there is a need for increasingly greater specialization or unbundling of the various services that is driven principally by the diversity of laws and ordinances that are relevant to each transaction and the differing structures utilized in each securitization project. Thus the greater division of roles now compared to earlier real estate transactions has led to an increasing number of participants in each transaction. One other factor that has made real estate securitization difficult to understand for Japanese speakers is the frequent use of non-Japanese terminology. We have compiled an overview of the market participants, their roles in real estate securitization and finance aspects to real estate securitization to serve as an introduction and assist in the understanding the roles of participants (Figure 1-3). Figure 1-3 Participants in Real Estate Securitization and Finance (SPC as the securitization vehicle) *Click the image, large size is available

Note) In this case, the vehicle does not own the real estate directly but rather owns the beneficiary interests in trust for the real estate 1) Originator 2) Investors Investors can be subdivided into debt investors and equity investors and each investor group has specific risk-return characteristics they aim for when investing in real estate securitization products. 3) Lender 4) Arranger The arranger is responsible for supporting and coordinating with third party consultants and contractors for preparing due diligence reports, engineering reports etc. and advises in the selection of various professional service providers including accountants, lawyers, real estate appraisers, trust banks and securities firms. After the asset is in the securitization vehicle the arranger may select the underwriter for the sale of public securities, if applicable, as well as the financing counterpart who will provide the nonrecourse loan and finally provide advice when considering disposing of the real estate. Generally, arrangers are securities firms, city banks, trust banks, other financial institutions, real estate companies and consultants. 5) Underwriter 6) Trust Banks The trust bank is a specialized institution that can handle a variety of functions for a real estate securitization; a trust bank can act as the arranger, lender, bond manager, asset custodian when the securitization vehicle issues corporate bonds and handle administrative duties. 7) Rating Companies Obtaining a rating from a rating agency increases the transparency of the securitization structure and improves the marketability of the securities that are issued, thus the fund raising becomes easier. 8) Asset Manager In situations where investors invest in an asset-management securitization, the asset manager is responsible for investing the funds invested by investors in real estate related assets and in such a case the asset manager may be referred to as the fund manager. 9) Property Manager There are cases where the asset manager also acts as the property manager or building and facility management firms that manage other buildings locally provide these services under contract. 10) Servicer 11) Administrative Affairs Manager 12) Lawyer 13) Certified Public Accountant and Auditor 14) Tax Attorney and Tax Attorney Corporation 15) Due Diligence Vendors |

|||

|

|||